Your AI roadmap is wrong: planning for a future you cannot predict

Bottom line: A traditional roadmap assumes a knowable future and commits to a sequence of milestones to reach it. AI moves too fast for that assumption to hold — capability you would build this quarter may be free next quarter, and a bet that looks safe today may be obsoleted by a model release. The answer is not a better roadmap but a different instrument: a portfolio of bets, sized and staged by uncertainty rather than a linear plan. You cannot plan a route through a future you cannot predict. You can only allocate across bets and rebalance as it arrives.

A roadmap is a forecast wearing a Gantt chart

A roadmap looks like a plan, but underneath it is a forecast. Every dated milestone is a prediction: that this capability will still be worth building when we reach it, that the problem will still look the way it looks now, that the world will hold still long enough for the sequence to play out. In stable domains that forecast is reasonable, and the roadmap is a sound instrument. In AI it is a liability, because the one thing the field reliably does is move faster than the plan — and a roadmap is a forecast that has been given the false authority of a Gantt chart, committing real budget and headcount to predictions that the next model release can invalidate overnight.

The cost of this shows up as a specific, recurring waste. A team commits to building a capability over two quarters; halfway through, a model release makes that capability available off the shelf, and the half-built bespoke version is now sunk cost defended by the very plan that created it. Or a milestone that looked central when the roadmap was drawn becomes irrelevant as the field moves, but it stays on the plan because plans have momentum and removing a committed item feels like failure. The high rate at which AI projects are abandoned is, in part, the sound of roadmaps colliding with a future they could not predict — committed plans meeting an uncommitted world.

A roadmap is a forecast that has been handed a Gantt chart's authority. In a field that moves this fast, that authority is exactly the problem.

Stop planning the route. Start sizing the bets.

The instinct, when a roadmap keeps being wrong, is to make a better roadmap — plan more carefully, forecast more precisely, add more detail. This is the wrong response, because the problem is not that the forecast was insufficiently detailed; it is that the future is genuinely unpredictable and no amount of detail fixes that. A more precise prediction of an unknowable future is just a more confident way to be wrong. The right response is to change instruments entirely: stop trying to plan the route and start managing a portfolio of bets.

This is the shift from planning under certainty to allocating under uncertainty, and it is a different discipline with different tools. A planner asks "what is the sequence of steps to the goal." A portfolio manager asks "how should I allocate across bets given that I cannot predict which will pay off." The second question is the right one for AI, because it does not require predicting the future — it requires sizing your exposure to different possible futures, which is a thing you can actually do. A portfolio does not commit to a route; it allocates across possibilities and rebalances as the world reveals which ones were right. That is a posture built for uncertainty rather than one defeated by it.

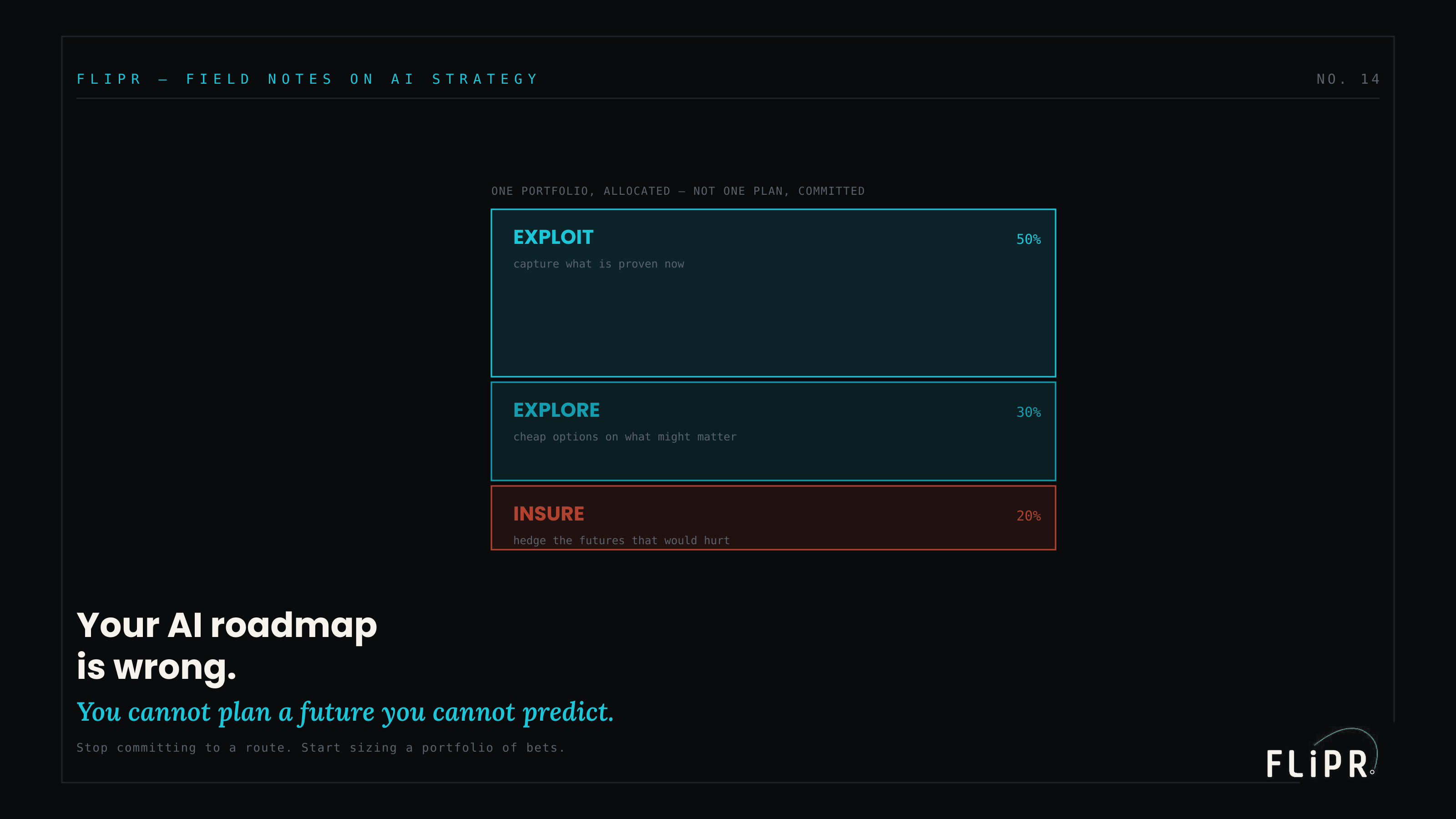

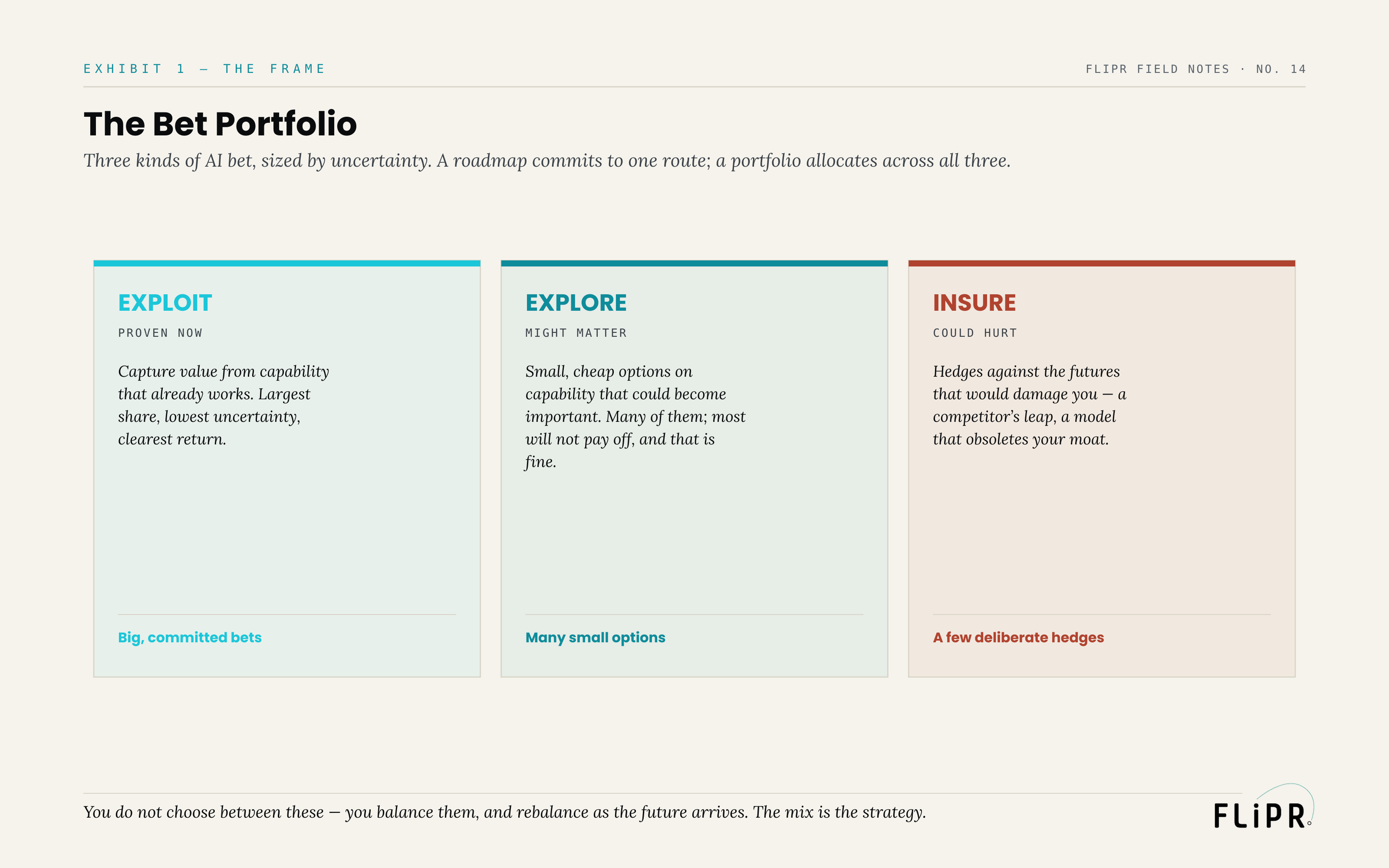

The Bet Portfolio

A portfolio has three kinds of bet, each sized by a different relationship to uncertainty.

Exhibit 1. Three kinds of AI bet, sized by uncertainty. A roadmap commits to one route; a portfolio allocates across all three.

Exhibit 1. Three kinds of AI bet, sized by uncertainty. A roadmap commits to one route; a portfolio allocates across all three.

Exploit bets capture value from capability that is already proven to work. These are your largest, most committed bets, with the lowest uncertainty and the clearest return — the things you know pay off, funded fully. Explore bets are small, cheap options on capability that might become important but has not yet. There are many of them, most will not pay off, and that is exactly right: each is an inexpensive ticket on a possible future, and you are buying optionality, not certainty. Insure bets are hedges against the futures that would hurt you — a competitor's leap, a model release that obsoletes your moat, a regulatory shift. There are only a few, and they are sized to the downside they protect against, not the upside they might produce. The mix of these three is your AI strategy, and unlike a roadmap, it does not commit to a single prediction. It spreads exposure across what is proven, what is possible, and what is dangerous.

The crucial property is that you do not choose between these bets — you hold all three at once and rebalance as the future arrives. When a model release validates an explore bet, you shift weight toward it. When the field moves against an insure scenario, you are already hedged. The portfolio adapts where a roadmap can only be wrong.

A roadmap makes one prediction and commits to it. A portfolio holds many bets at once and lets the future decide the winners. Only one of those survives a surprise.

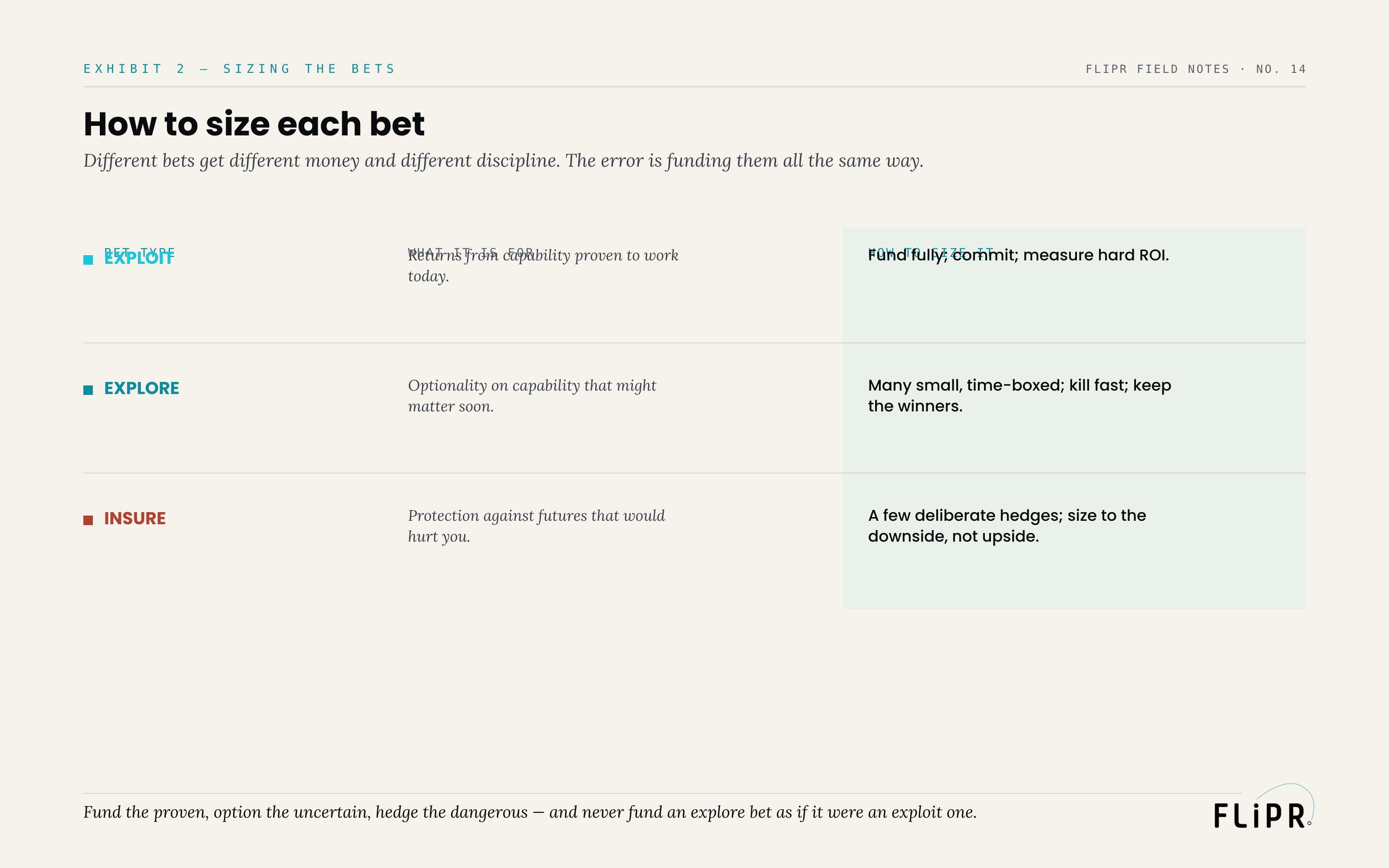

Sizing and staging each bet

The three kinds of bet get different money and different discipline, and the most common error is funding them all the same way.

Exhibit 2. Different bets get different money and different discipline. The error is funding them all the same way.

Exhibit 2. Different bets get different money and different discipline. The error is funding them all the same way.

Exploit bets are for returns from capability proven to work today, so you fund them fully, commit, and measure them on hard ROI — these are real investments with real expected payoffs. Explore bets are for optionality on capability that might matter soon, so you fund many of them small and time-boxed, kill them fast when they do not pan out, and keep the few that do — the discipline is cheapness and ruthlessness, not commitment. Insure bets are for protection against futures that would hurt you, so you make a few deliberate hedges sized to the downside rather than the upside — you are buying protection, not chasing return. The failure mode is mixing these up: funding an explore bet as if it were an exploit one (pouring committed budget into an unproven option), or sizing an insure bet by its upside (turning a hedge into a speculative bet). Each bet type has its own logic, and applying the wrong one is how a portfolio quietly turns back into a roadmap — a pile of over-committed bets pretending to be options.

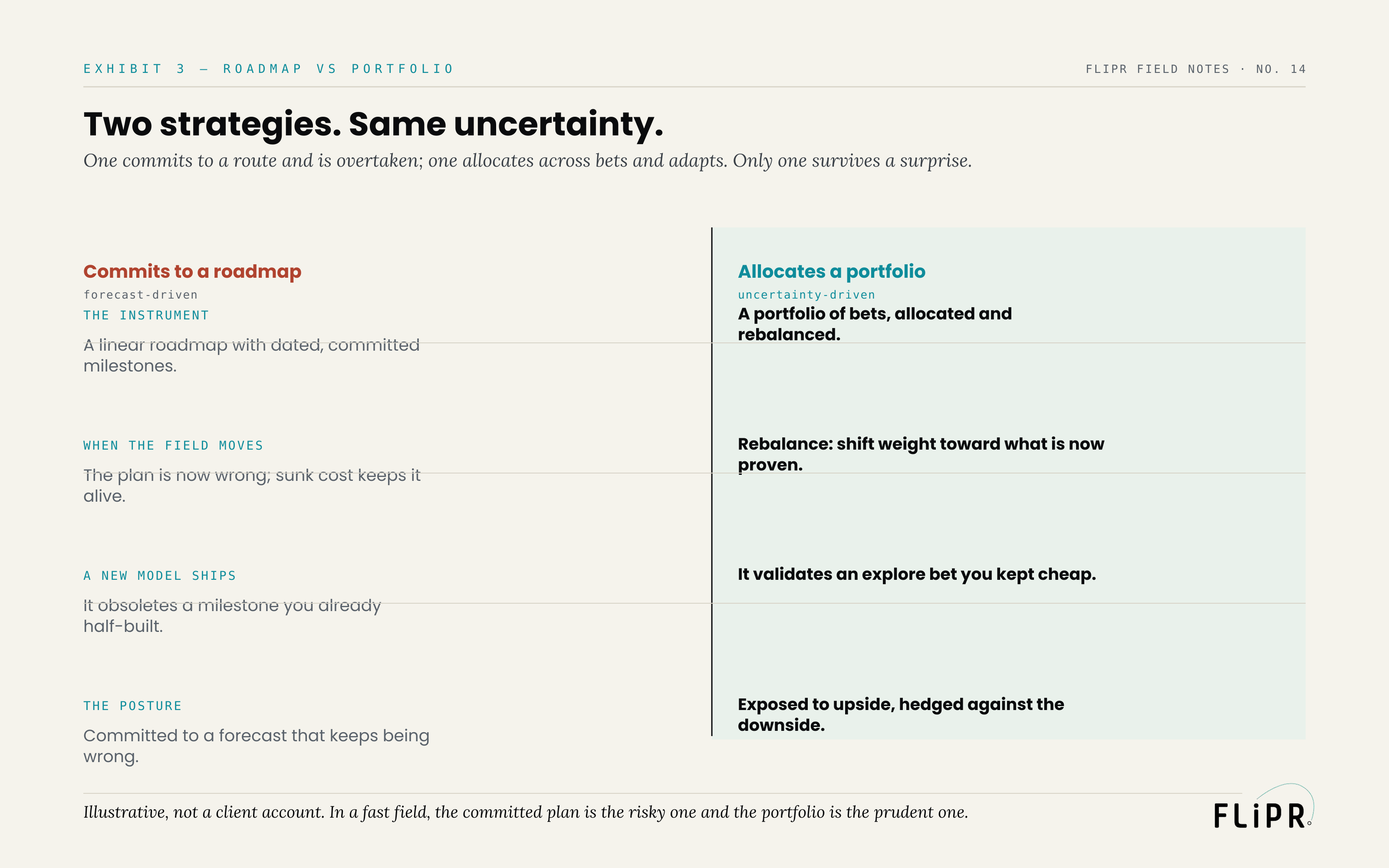

What this looks like on Monday

Put two strategies side by side, facing the same uncertainty. (This is an illustration, not an account of any specific engagement.)

Exhibit 3. One commits to a route and is overtaken; one allocates and adapts. Illustrative, not a client account.

Exhibit 3. One commits to a route and is overtaken; one allocates and adapts. Illustrative, not a client account.

The first commits to a roadmap: a linear plan with dated, committed milestones. When the field moves, the plan is now wrong, but sunk cost keeps it alive — the team finishes building things because they were on the plan, not because they still make sense. When a new model ships, it obsoletes a milestone the team already half-built. The posture is one of commitment to a forecast that keeps being wrong, and each surprise is a loss.

The second allocates a portfolio: bets sized and staged by uncertainty, rebalanced as the world changes. When the field moves, the team rebalances, shifting weight toward what is now proven. When a new model ships, it validates an explore bet the team had deliberately kept cheap — a win, not a loss, because the exposure was sized for exactly that possibility. The posture is one of being exposed to the upside and hedged against the downside, and each surprise is information the portfolio can act on.

Same uncertainty, same field. One strategy committed to a route and was overtaken by it; the other allocated across bets and adapted — and only one was still standing after the surprise.

Where this argument runs out

This frame has limits, and they cut in more than one direction.

Some things genuinely do need a committed roadmap, and treating everything as a rebalanceable bet is its own failure. Foundational infrastructure, regulatory commitments, and multi-year platform decisions require commitment to be built at all, and a portfolio posture that refuses to ever commit will never build the durable things that need a plan — the portfolio is for the uncertain layer of AI strategy, not for every decision in the business. There is also a real risk of mistaking a portfolio for an absence of strategy: "we hold many bets and rebalance" can become an excuse for dithering, for never committing to anything, for a scattered collection of half-funded experiments that add up to no direction at all. A portfolio is a strategy — a deliberate allocation with a thesis behind each bet — not a way to avoid having one. And rebalancing has a cost; thrashing the portfolio with every news cycle is as damaging as never adjusting it, so the discipline is to rebalance on genuine signal, not on noise. Finally, explore bets can quietly become permanent R&D — perpetually funded, never killed, never scaled — which defeats their purpose; an option you never exercise or expire is just a slow leak.

That bounds the claim. Commit where commitment is genuinely required, hold a real thesis behind each bet rather than dithering, rebalance on signal rather than noise, and force explore bets to either graduate or die. The point is not to never commit; it is to stop committing your whole strategy to a forecast in a field that punishes forecasts.

The decision

So the move, before you next publish an AI roadmap, is concrete.

Replace the linear plan with a portfolio: sort your AI investments into exploit, explore, and insure, and size each by its own logic — fund the proven fully, option the uncertain cheaply and in volume, hedge the dangerous deliberately. Put a real thesis behind each bet so the portfolio is a strategy and not a scatter, and set a rebalancing cadence so you adjust on genuine signal as the field moves rather than thrashing on noise or freezing on momentum. Force every explore bet to carry a graduation-or-death criterion so your options do not rot into permanent R&D. And reserve committed, roadmap-style planning for the genuinely foundational decisions that require it.

The future of AI capability is not knowable on the timeline your roadmap commits to, and a more detailed forecast of an unpredictable future is just a more confident error. Hold a portfolio instead of a plan, allocate across what is proven, possible, and dangerous, and rebalance as the world tells you which bets were right. In a field that moves this fast, the committed roadmap is the risky instrument and the portfolio is the prudent one. How you cost each bet is the discipline from the companion piece on the CFO business case; how each bet graduates from option to scaled investment is the gradient from the piece on the pilot trap.

Sources

- Stanford HAI — Artificial Intelligence Index Report 2025. The pace of capability advance and cost decline that makes long-horizon AI commitments fragile. https://aiindex.stanford.edu/report/

- Gartner. Public projection on the high rate at which generative AI projects are abandoned — a cost partly attributable to over-committed plans. https://www.gartner.com/en/newsroom

- MIT NANDA — The State of AI in Business 2025. Finding that most enterprise GenAI pilots show no measurable return, consistent with committing before value is proven.

Bottom-line summary (one line)

AI moves too fast for a committed roadmap, so replace the linear plan with a Bet Portfolio — exploit what's proven, explore what might matter cheaply, insure against what would hurt — and rebalance on real signal as the unpredictable future arrives.

Suggested LinkedIn hooks (link back to the blog)

- Your AI roadmap is a forecast wearing a Gantt chart. In a field this fast, that borrowed authority is exactly the problem — you're committing budget to predictions a model release can void. [link]

- Stop planning the route; start sizing the bets. A roadmap makes one prediction and commits. A portfolio holds many bets and lets the future decide. Only one survives a surprise. [link]

- Three kinds of AI bet: exploit what's proven, explore what might matter, insure against what would hurt. Fund them differently — and never fund an explore bet like an exploit one. [link]